Most businesses use either FIFO or LIFO, and sole proprietors typically use average cost. Keeping track of all incoming and outgoing inventory costs is key to accurate inventory valuation. what is a simple tax return Try FreshBooks for free to boost your efficiency and improve your inventory management today. FIFO and LIFO are two common methods businesses use to assign value to their inventory.

The FIFO Method: First In, First Out

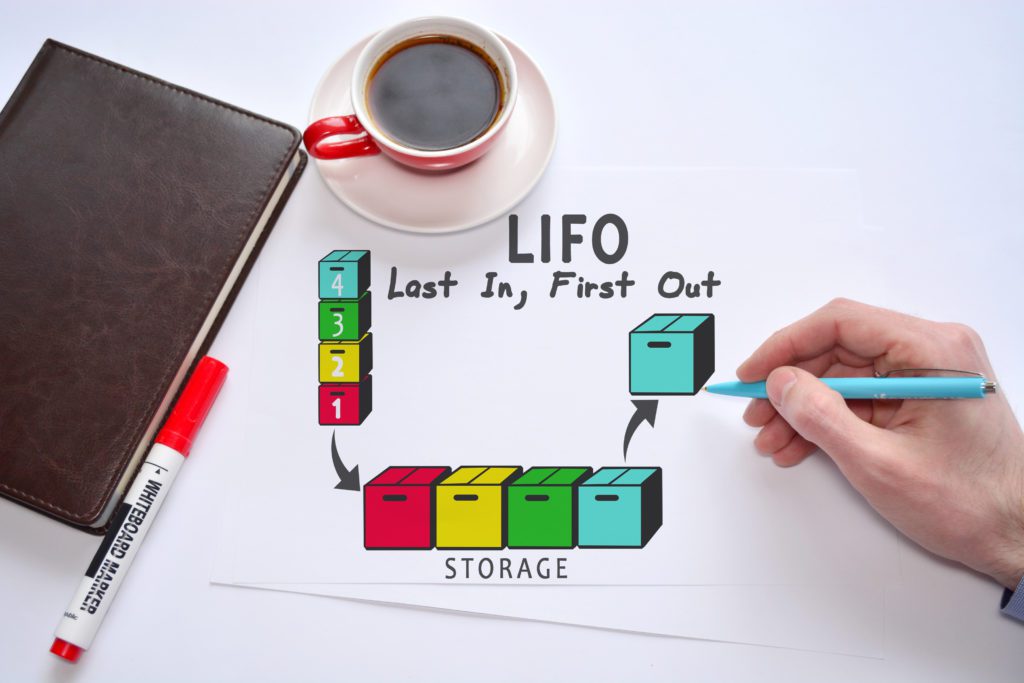

Although a business’s real income and profits are the same, using FIFO or LIFO will result in different reported net income and profits. Average cost inventory is another method that assigns the same cost to each item and results in net income and ending inventory balances between FIFO and LIFO. Based on the LIFO method, the last inventory in is the first inventory sold.

Tax Planning

LIFO, on the other hand, can reduce taxes during inflation but adds complexity and isn’t accepted under global accounting standards. Consider your inventory type, tax strategy, and accounting requirements when deciding. When you’re in an inflationary period and prices are rising, LIFO can help you manage your increasing costs. On the other hand, FIFO is more likely to show higher profits on paper because it uses the older, cheaper costs.

Why would businesses use last in, first out (LIFO)?

On the other hand, LIFO can lower your taxable income by referencing the most recent, higher-cost inventory. As LIFO isn’t accepted under international accounting standards (IFRS), not all companies can use this method. LIFO, on the other hand, offers a strategic tax advantage by aligning the cost of goods sold with current market prices. This results in lower taxable income during periods of rising prices, effectively reducing the company’s tax liability. The tax savings can be reinvested into the business, fostering innovation, expansion, or debt reduction. However, it’s important to note that LIFO is not permitted under International Financial Reporting Standards (IFRS), limiting its use to companies that primarily report under U.S.

- In contrast, using the FIFO method, the $100 widgets are sold first, followed by the $200 widgets.

- In a similar vein, it’s worth mentioning FEFO (First Expired, First Out), which is very similar to FIFO, but specifically works based on expiry dates of goods.

- FIFO is also generally considered to be a more accurate and reliable inventory valuation method since it is more difficult to misrepresent costs.

- The same example used earlier can be used to show the LIFO method for calculating the cost of goods sold.

Other common accounting methods

For many companies, inventory represents a large, if not the largest, portion of their assets. Therefore, it is important that serious investors understand how to assess the inventory line item when comparing companies across industries or in their own portfolios. Kristen Slavin is a CPA with 16 years of experience, specializing in accounting, bookkeeping, and tax services for small businesses. A member of the CPA Association of BC, she also holds a Master’s Degree in Business Administration from Simon Fraser University. In her spare time, Kristen enjoys camping, hiking, and road tripping with her husband and two children.

How To Calculate FIFO and LIFO

You neither want to understate nor overstate your business’s profitability. This is why choosing the inventory valuation method that is best for your business is critically important. The best choice between LIFO and FIFO depends on your business needs and financial goals. FIFO is ideal for managing perishable goods and provides a straightforward approach, making it widely accepted, including internationally.

A company’s recordkeeping must track the total cost of inventory items, and the units bought and sold. FIFO will have a higher ending inventory value and lower cost of goods sold (COGS) compared to LIFO in a period of rising prices. Therefore, under these circumstances, FIFO would produce a higher gross profit and, similarly, a higher income tax expense. A company might use the LIFO method for accounting purposes, even if it uses FIFO for inventory management purposes (i.e., for the actual storage, shelving, and sale of its merchandise). However, this does not preclude that same company from accounting for its merchandise with the LIFO method. In addition to being allowable by both IFRS and GAAP users, the FIFO inventory method may require greater consideration when selecting an inventory method.

It’s also the most accurate method of aligning the expected cost flow with the actual flow of goods. It reduces the impact of inflation, assuming that the cost of purchasing newer inventory will be higher than the purchasing cost of older inventory. The company’s accounts will better reflect the value of current inventory because the unsold products are also the newest ones.

The remaining inventory assets are matched to assets that were most recently purchased or produced. FIFO is the most popular inventory method because it’s unrestricted for U.S.- or international-based companies and it increases the value of purchased inventory. In the FIFO method, the initial purchasing cost is subtracted from its selling price to calculate the reported profit.

The FIFO vs. LIFO accounting decision matters because of the fact that inventory cost recognition directly impacts a company’s current period cost of goods sold (COGS) and net income. With FIFO, the cost of inventory reported on the balance sheet represents the cost of the inventory purchased earliest. FIFO most closely mimics the flow of inventory, as businesses are far more likely to sell the oldest inventory first. The FIFO method can result in higher income taxes for a company because there’s a wider gap between costs and revenue. The alternate method of LIFO allows companies to list their most recent costs first in jurisdictions that allow it.